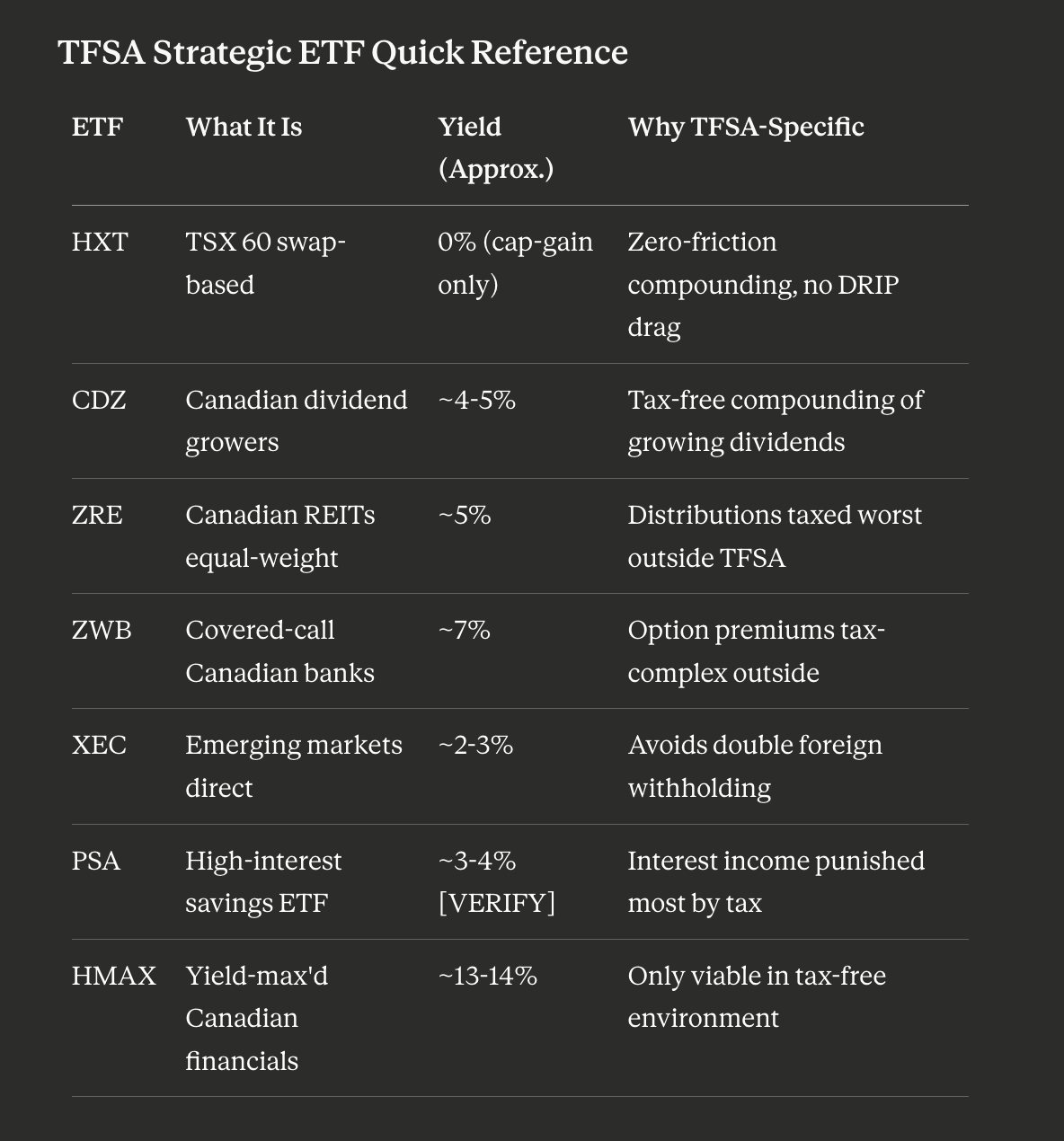

7 Strategic ETFs for a Canadian TFSA (That Nobody Talks About)

If you've already read ten "best ETFs for your TFSA" posts, you've already met XEQT, VEQT, VFV and XIC. This post is the other list, the one that takes the TFSA's actual tax mechanics seriously and points to seven ETFs that are uniquely correct inside a TFSA and meaningfully wrong almost everywhere else. Each pick exists because of a specific tax quirk, not because of a star rating.

The unifying idea is simple: outside a TFSA, the type of income you earn determines how much tax you pay. Interest is taxed at full marginal rates. Foreign dividends face withholding. Canadian eligible dividends get a credit. Capital gains are 50% included. Return of capital just adjusts your cost base. Inside a TFSA, none of that matters. Every dollar is treated identically: zero. That makes the TFSA's highest-value use the exact opposite of what most Canadians do with it. The income types that get punished hardest elsewhere are the ones that benefit most from TFSA shelter.

That logic produces a very different list of ETFs than the standard one.

How Should You Think About ETF Selection Inside a TFSA?

Two questions, asked in order.

First: what income type would this ETF generate, and how badly would that income be taxed outside a TFSA? REIT distributions, covered call premiums, interest, and high-yield Canadian dividends all get punished outside the shelter. They are the most TFSA-deserving holdings.

Second: does the structure of the ETF leak tax even inside a TFSA? US-listed ETFs face 15% unrecoverable withholding on US dividends. International exposure routed through a US-listed wrapper inside a Canadian ETF gets hit by two layers of foreign withholding. Holding the underlying stocks directly through a Canadian-listed ETF eliminates the second layer.

Those two questions get you to a strategically different portfolio than the standard all-in-one stack. Below are seven ETFs that answer both questions well.

The 7 Strategic TFSA ETFs

1. HXT (Global X S&P/TSX 60 Index Corporate Class ETF)

MER: ~0.08%

The cheapest broad Canadian exposure on the market, and structurally different from XIC or VCN in a way most posts gloss over. HXT uses a total return swap rather than holding the underlying TSX 60 stocks. There are no dividend distributions. The full return compounds inside the unit price.

Inside a TFSA the dividend question is moot anyway, since Canadian dividends are already tax-free. The real win is operational: no dividend cash piling up between purchases, no DRIP friction, no rounding losses on partial shares. Over 30 years on a maxed TFSA the auto-compounding edge is meaningful.

The honest caveat: counterparty risk. The swap is with National Bank. Realistically a small tail risk for one of Canada's Big Six, but not zero. The CRA has also periodically signalled discomfort with the structure, though it has never actually challenged it. If either of those risks bothers you, XIC or VCN are the more conservative substitutes.

HXT ETF portfolio holding breakdown by sector and geography.

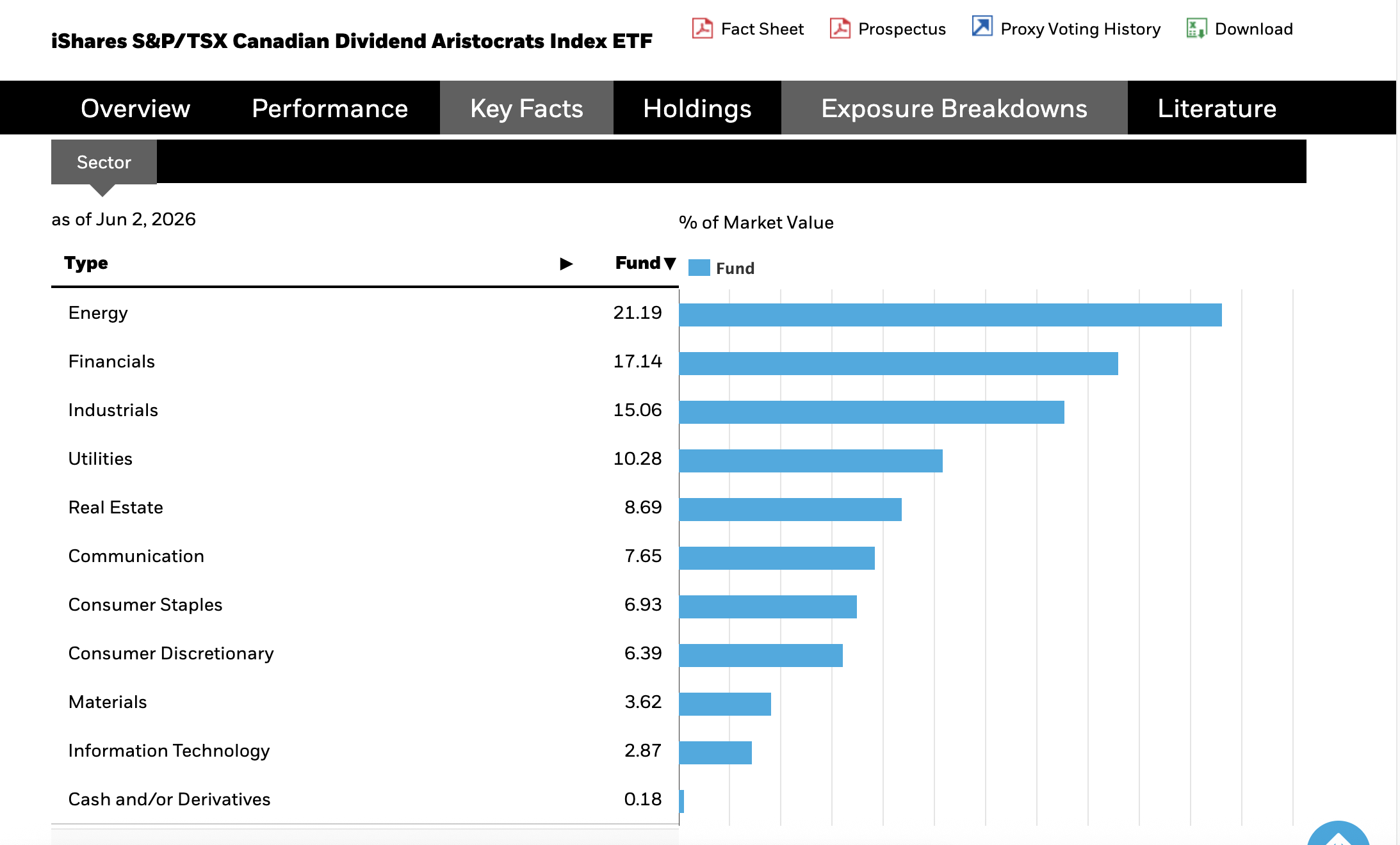

2. CDZ (iShares S&P/TSX Canadian Dividend Aristocrats Index ETF)

MER: ~0.66%

A 4-5% yield from Canadian companies that have grown their dividends for at least five consecutive years. Heavy weighting in financials, utilities, pipelines, and REITs.

The TFSA logic is straightforward and overlooked. In a non-registered account you'd pay tax on those distributions every year, partially offset by the Canadian dividend tax credit but still real money. In an RRSP, you'd eventually pay full marginal rate on withdrawal. Only inside a TFSA does the entire dividend stream and its growth compound tax-free forever.

The DIY-finance crowd is structurally allergic to dividend strategies because they associate them with retirees and Jim Cramer. The math on dividend-growers held in a TFSA is actually exceptional. Total return over 30 years can rival broad-market because every dollar of yield compounds with zero leakage.

The counterargument worth airing: sector concentration. Banks, pipelines, and utilities are all rate-sensitive. 2022 was brutal for this category. CDZ is not a stand-alone portfolio.

CDZ ETF portfolio holding breakdown by sector.

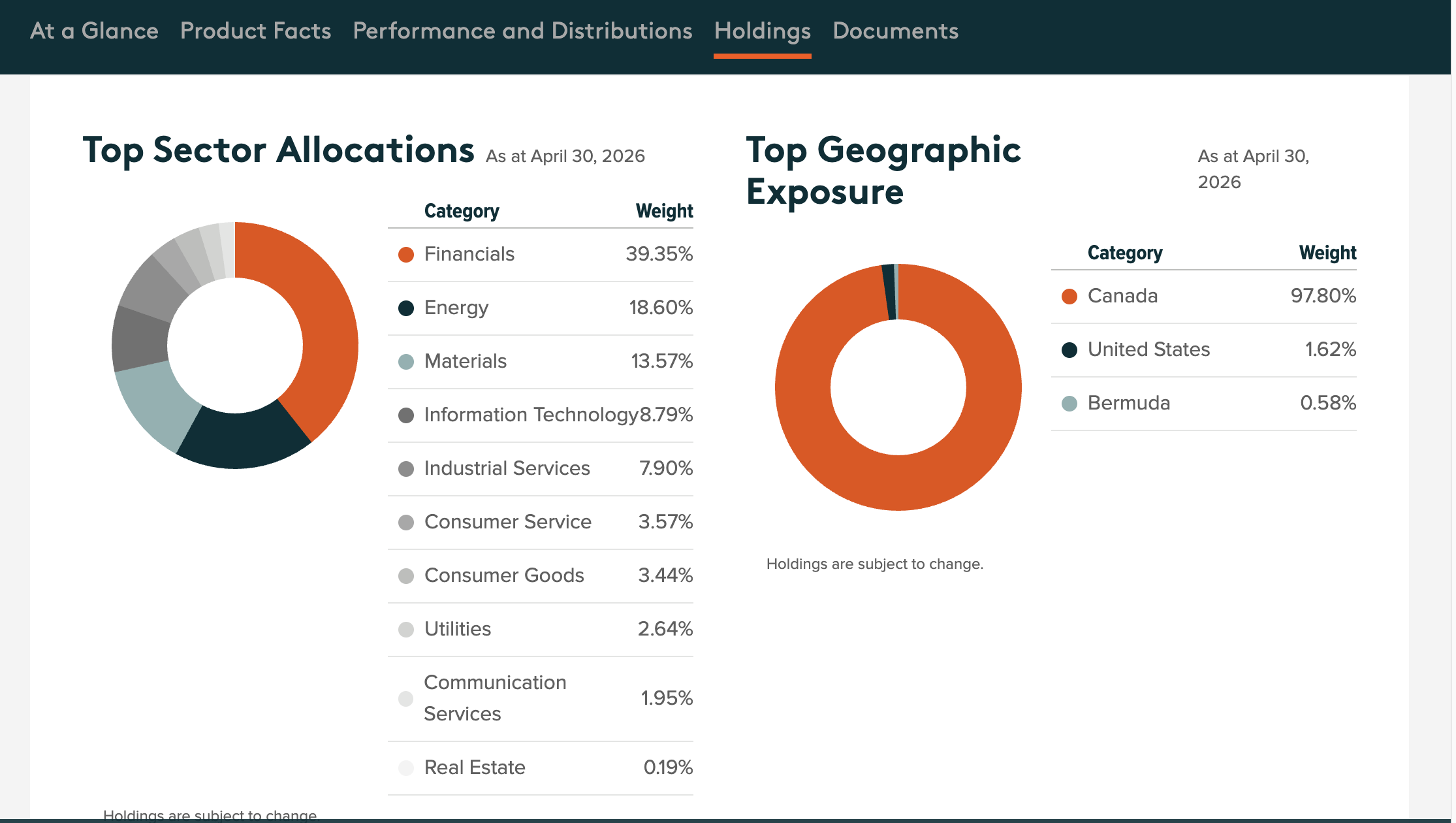

3. ZRE (BMO Equal Weight REITs Index ETF)

MER: ~0.61%

Equal-weighted Canadian REIT exposure with a roughly 5% yield. This is one of the most TFSA-optimal asset classes that exists.

REIT distributions are not eligible dividends. They are a mix of rental income (taxed at full marginal rates), return of capital (which just reduces your adjusted cost base and is taxed as capital gain on eventual sale), and sometimes capital gains. Held in a non-registered account, this creates a tax-reporting headache and burns through return at full marginal rates. Held in a TFSA, none of that matters. The TFSA is the only account where REITs are tax-equivalent to broad-market equity.

The asymmetry is meaningful. An Ontario investor at the top marginal bracket holding ZRE outside a TFSA gives up close to two full percentage points of annual return to tax. Inside the TFSA, they get the full distribution.

Canadian REITs have been a poor performer this past decade because of rates. Treat ZRE as a contrarian rate-sensitive holding, not a growth play.

ZRE ETF historical performance chart.

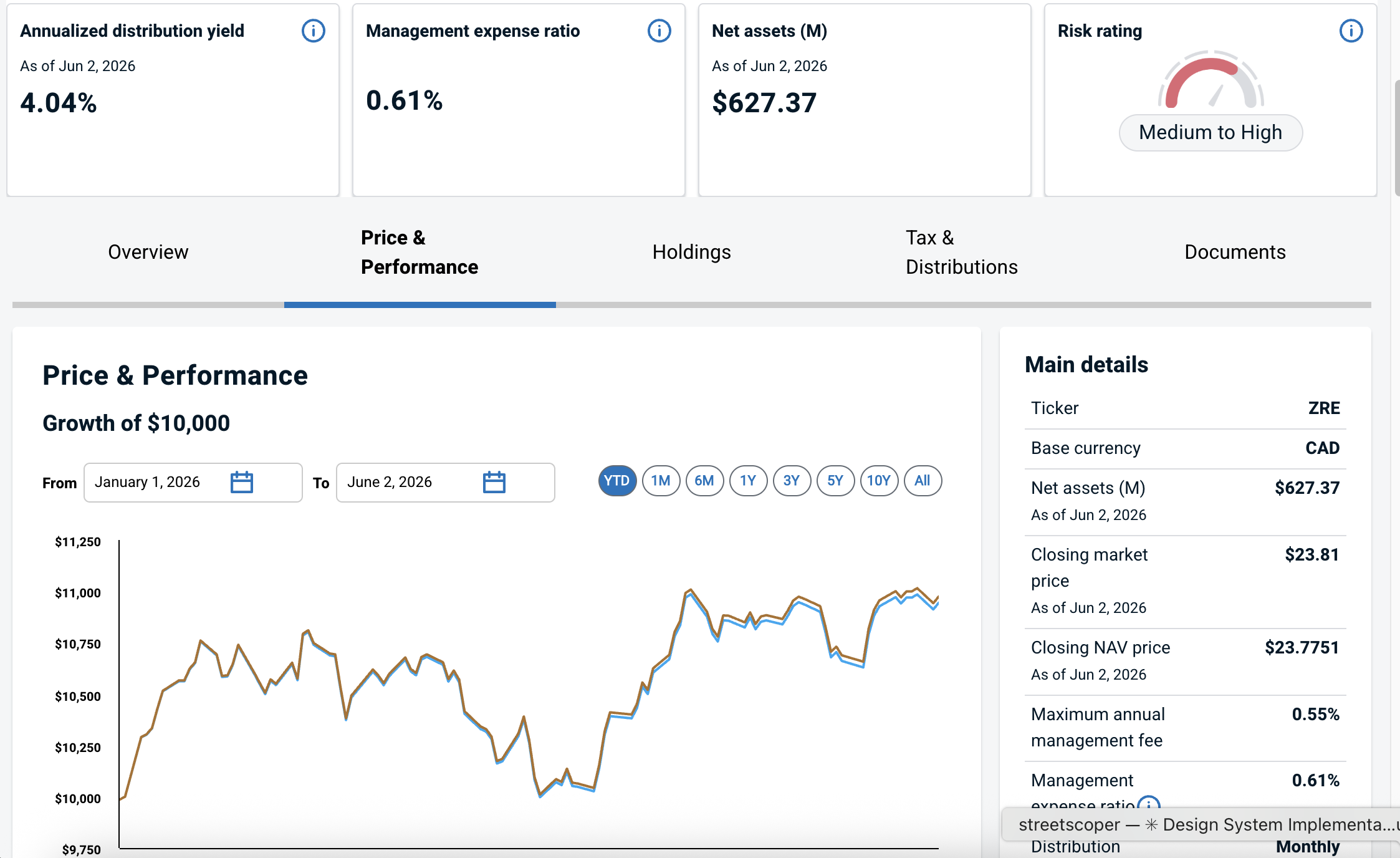

4. ZWB (BMO Covered Call Canadian Banks ETF)

MER: ~0.72%

Yield around 7%, generated partly from Canadian bank dividends and partly from selling covered call options against the underlying positions. Sister product ZWU does the same on utilities.

The mechanics matter. Covered call ETFs trade upside for current income. The option premiums are partly classified as capital gains for tax purposes, which is complicated to report outside a TFSA. Inside one, the classification is irrelevant. The whole distribution is tax-free.

This is the controversial pick. Nearly every Canadian personal-finance YouTuber will tell you covered call ETFs are a scam. They're not wrong for accumulators, ZWB underperforms ZEB (its non-covered-call sibling) on total return because the covered calls cap upside in rallies. They are wrong if the goal is distribution rather than accumulation. For a near-retiree or anyone using their TFSA for tax-free monthly cash flow, ZWB's 7% sustainable yield from the most defensible sector in the Canadian economy is a legitimate strategy.

The right framing: ZWB is wrong for a 30-year-old maxing out their TFSA. It is right for a 60-year-old drawing income from one.

ZWB ETF yield source breakdown

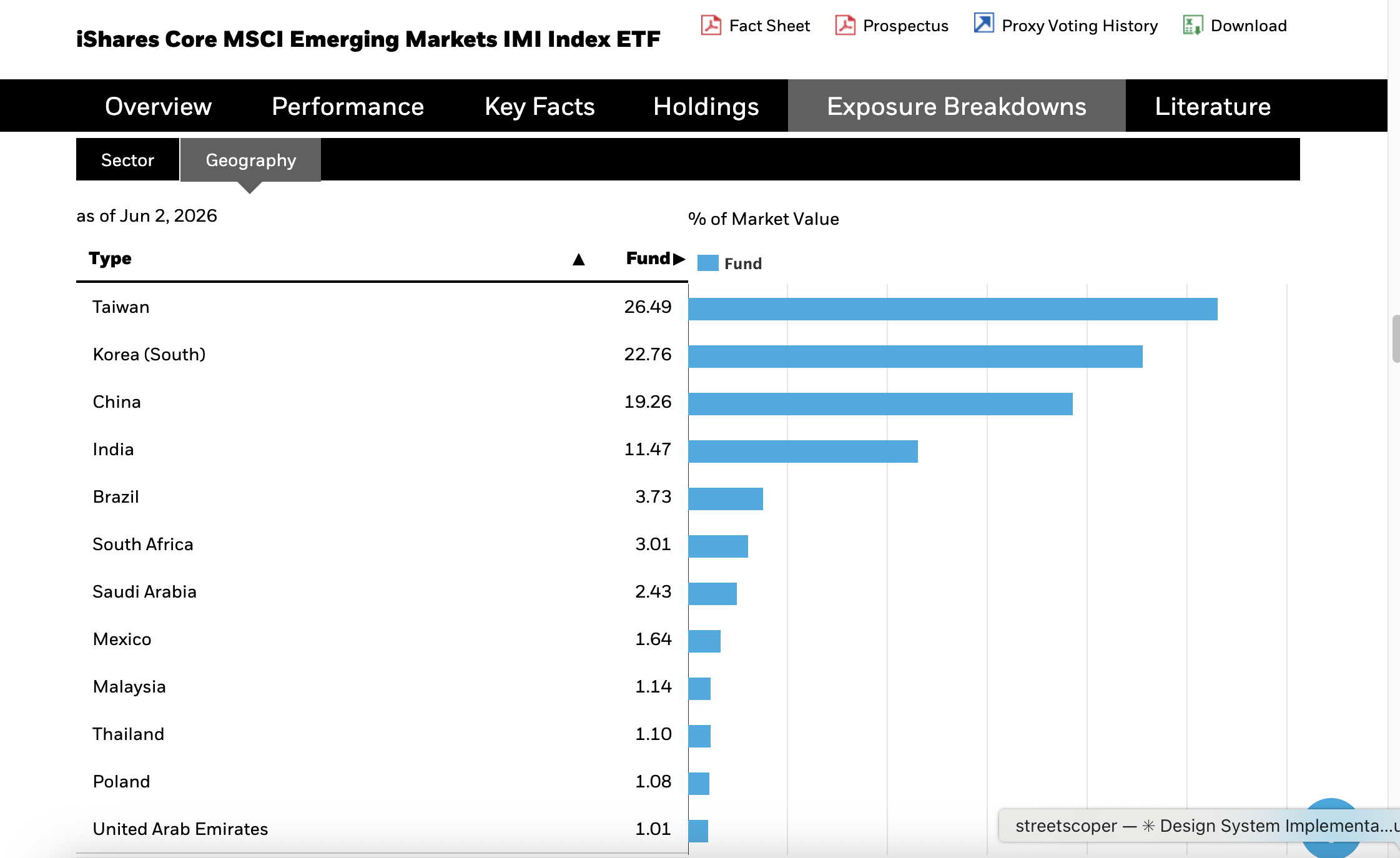

5. XEC (iShares Core MSCI Emerging Markets IMI Index ETF)

MER: ~0.28%

The underrated structural argument for emerging markets in a TFSA has nothing to do with returns and everything to do with stacked withholding tax.

Emerging-market countries impose their own withholding taxes on dividends. Brazil, India, Taiwan, and China all withhold 10-30% at source. When you hold EM exposure via a US-listed ETF (VWO, IEMG, etc.) inside a TFSA, you face double withholding: first the source country, then the US when the ETF distributes to you. Neither layer is recoverable.

XEC holds the underlying EM stocks directly. The source-country withholding still happens inside the fund, you can't avoid that. But the second US layer is eliminated entirely. For a Canadian holding EM in a TFSA, this can be worth 50+ basis points a year over a US-listed alternative.

EM has been a 15-year underperformer. Treat XEC as a contrarian, tax-efficient diversifier, not a return-chasing trade.

XEC ETF geographic breakdown of portfolio.

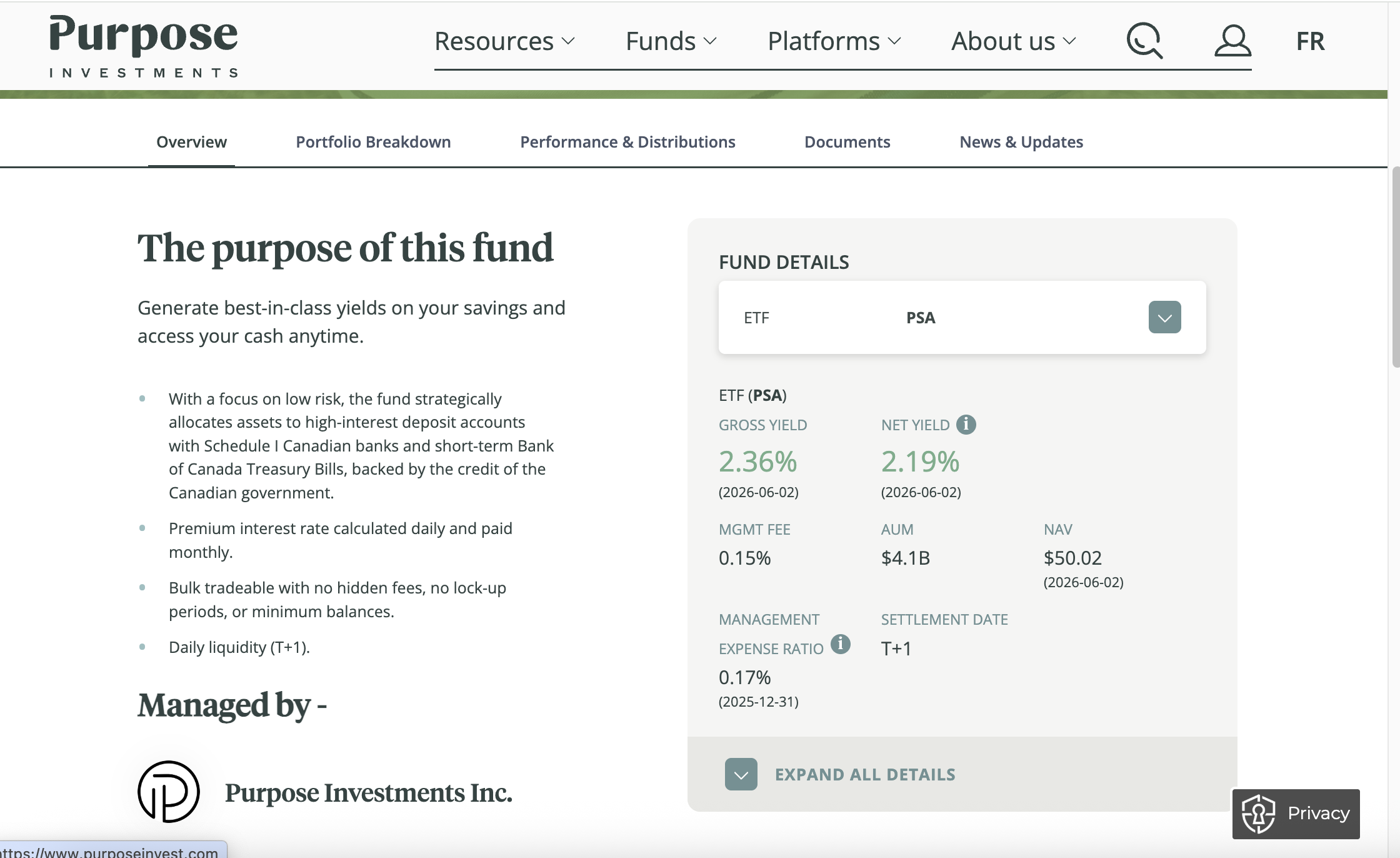

6. PSA (Global X High Interest Savings ETF)

MER: ~0.17%

The pick that exposes the single most common TFSA mistake in Canada.

Millions of Canadians hold tens of thousands of dollars in high-interest savings accounts at EQ Bank, Tangerine, or Wealthsimple Cash, earning 2.5-4% interest fully taxed at marginal rates. Meanwhile their actual TFSA at a brokerage sits half-funded or invested in equities that generate negligible income.

That's the wrong way around. Interest is the most tax-punished income type. An Ontario resident at $100K income pays roughly 43% marginal tax on every dollar of interest, dropping the effective return on a 3.5% HISA to about 2%. PSA pays a comparable rate to the best HISAs in Canada with T+1 liquidity, and held inside a TFSA every basis point is yours.

The standard advice is "never hold cash in a TFSA, you're wasting growth potential." That advice is correct for money you actually want invested. It is wrong for cash you need liquid anyway. If you're going to hold $30K in a HISA somewhere, holding it in PSA inside your TFSA is mathematically superior to holding it in any taxable HISA, full stop.

PSA ETF dividend yield.

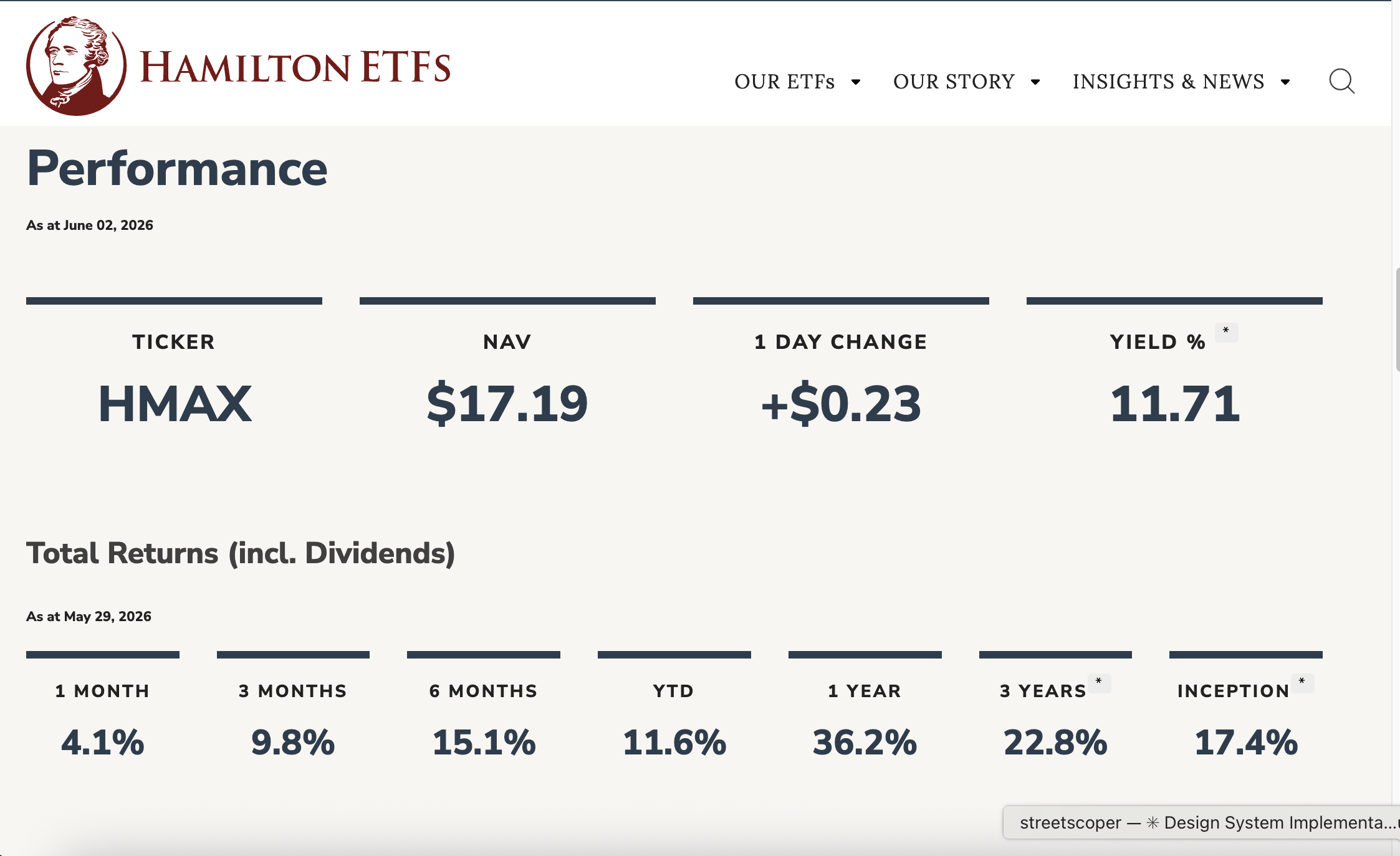

7. HMAX (Hamilton Canadian Financials Yield Maximizer ETF)

MER: ~0.65%

The most aggressive pick on this list, and the one most clearly engineered for a TFSA.

HMAX uses a covered call overlay on Canadian financials (the Big Six banks plus the largest insurers) to push the distribution yield into the 13-14% range. In any taxable account this is a structural disaster: high-frequency distributions, complex option-premium tax treatment, and tax drag that crushes after-tax returns. In a TFSA, none of those problems exist.

This is not a recommendation to buy HMAX. It is a recommendation to understand that the TFSA is the only place this kind of yield strategy is mathematically viable. If you understand the trade you're making (upside cap on bank stocks in exchange for outsized current income), the TFSA is the only Canadian account where the math works.

HMAX is for income generation, not capital growth. Total return will likely lag ZEB or even just owning RY, TD, and BNS directly over a long horizon. The case for HMAX is "I want monthly tax-free cash flow from Canadian banks and I'm willing to give up some upside to get it." For that specific goal, in that specific account, it's a defensible choice.

HMAX ETF historical performance & returns.

What Do These ETFs Have in Common?

Two things.

7 Strategic TFSA ETFs for Canadian Investors.

One: every distribution dollar is taxed harder outside a TFSA than inside one. That's the basic eligibility test for whether an ETF deserves precious TFSA contribution room. A pure capital-gains play (Berkshire Hathaway, QQC.F, single growth stocks) can compound in a non-registered account at the same effective tax rate it would inside a TFSA, especially if you never sell. A high-distribution holding cannot. The TFSA is wasted on the former and made for the latter.

Two: each pick has a real, sometimes ugly, tradeoff. HXT carries counterparty risk. CDZ is sector-concentrated. ZRE has been a poor performer for years. ZWB caps upside. XEC depends on EM rebounding. PSA earns the same as a HISA, no more. HMAX is structurally limited on total return. None of these are slam-dunk core holdings the way XEQT is. They are deliberate strategic allocations for specific reasons.

Where Should You Buy These ETFs?

All seven ETFs trade commission-free at Wealthsimple, Questrade, Qtrade, Moomoo, Webull, and NBDB. Most major Canadian brokers carry the full lineup since all seven trade on the TSX.

At a Big Bank brokerage (TD, RBC, BMO, CIBC, Scotia) you'll pay between $6.95 and $9.99 per buy. On a $500 position that's a 1.4-2% commission. On a strategic income holding like ZRE or HMAX where part of the case is the steady stream of distributions, paying $9.99 to reinvest each one destroys the math. Use a commission-free broker.

For a fuller comparison of commission-free brokers in Canada, see the master broker comparison and the best sign-up bonuses for new Canadian investors.

Are These ETFs Right for Every Canadian?

No. This list is explicitly not a portfolio. It's a menu of strategic positions that pair with a core all-in-one holding (XEQT, VEQT, or HEQT) or with a more conventional three-fund stack of VFV, XIC, and XEF.

A reasonable strategic TFSA might be 70% XEQT plus a 30% sleeve drawn from this list, weighted toward whatever income or tax mechanic best suits the investor. A 28-year-old building wealth probably skips ZWB, HMAX, and PSA entirely and overweights HXT and CDZ. A 58-year-old planning income probably does the opposite. The TFSA's flexibility is that both portfolios are tax-optimal, just for different goals.

Broker Guide Canada may earn a commission through affiliate links. This does not influence our editorial rankings. See our full disclosure.

FAQ

Are these ETFs better than XEQT?

No, they are different from XEQT. XEQT is a complete all-in-one global equity portfolio. The seven ETFs on this list are strategic positions designed to exploit specific TFSA tax mechanics. The right relationship is XEQT (or a similar all-in-one) as a core, with one or two of these as satellite holdings.

Can I hold all seven of these in my TFSA?

You can, but the result would be a heavily Canada-tilted, income-heavy portfolio with limited global equity exposure. That's a defensible portfolio for a near-retiree focused on tax-free Canadian income. It is a poor portfolio for a long-term accumulator. Mix with broad global equity exposure.

Why doesn't this list include VFV, VEQT or XEQT?

Because those are the standard answers in every other TFSA ETF article. This post is the second-layer answer for Canadians who already know about the basics and want to optimize further.

Is the CRA going to challenge HXT's swap structure?

It hasn't yet. The CRA has periodically signalled discomfort with total-return swap structures used to convert dividend income into capital gains for tax purposes. The risk is non-zero. For a TFSA holder this matters less than for a non-registered investor, because the distinction between dividend and capital gain inside a TFSA is irrelevant for tax. But if the structure were ever forced to change, unit-holders could face an unexpected tax event. Hold size accordingly.

Why is HMAX considered "strategic" and not just a yield trap?

Because in a TFSA the tax math changes what counts as a trap. Outside the TFSA, the high distribution is largely consumed by taxes, leaving thin after-tax return. Inside the TFSA, the full 13-14% lands in your hands. The structural giveaway, that covered call overlays cap upside in rallies, is still real and worth understanding. HMAX is a deliberate tradeoff, not a free lunch.