Wealthsimple Review 2026:

Last updated June 2026

Wealthsimple has the best app and the gentlest learning curve in Canada, commission-free stocks and ETFs, $0 options, and the only direct crypto from a major broker. It is the easiest place to start. The limits are reach and depth: a 1.5 percent currency exchange fee on the base tier, no bonds or international markets, and thin research.

Data verified June 2026Is Wealthsimple Worth It? The Bottom Line Up Front

Wealthsimple earns a 7.1 out of 10 and is the best starting point for most new and mainstream Canadian investors. Its all-in-one design is the real draw: investing, saving, crypto, and a chequing-style account in one excellent app. You pay no commissions on Canadian and US stocks and ETFs, nothing to trade options, and you can buy fractional shares, set up recurring investing, and hold crypto directly, which no other major Canadian broker offers. The trade-offs are a 1.5 percent currency fee on the base tier, a deliberately narrow product range, and research tools that are thin next to the rest of the field.

Who Is Wealthsimple For, and Who Should Skip It?

- New and mainstream investors who want the simplest, best-designed app and the gentlest learning curve in Canada.

- People who want their money in one place, investing, saving, crypto, and a spending account in a single app.

- Cost-conscious investors who want commission-free stocks and ETFs, $0 options, and low margin rates.

- Anyone who wants to buy fractional shares, invest small amounts on a schedule, or hold cryptocurrency directly.

- Investors who want bonds, GICs, mutual funds, or direct access to international markets, Wealthsimple offers none of these.

- Research-driven investors who rely on screeners, analyst data, and deep charting.

- Frequent US traders on the base tier who want to avoid the 1.5 percent currency fee without upgrading.

- Anyone who prioritizes top-rated customer support.

For the investors in that second list there are better-suited options, which you can compare in our master comparison table.

Wealthsimple at a Glance

On the base Core tier, Wealthsimple charges 1.5 percent to convert Canadian dollars to US dollars. On a $10,000 conversion that is about $150. Premium and Generation clients get a free US dollar account that avoids per-trade conversion.

What Are Wealthsimple's Fees?

Wealthsimple is genuinely low-cost for its core audience, with the currency fee on the base tier as the main thing to plan around.

The cheapest options trading in Canada

Canadian and US listed stocks and ETFs trade at $0, both ways, and options trade at $0 with no per-contract fee, the only broker in Canada at zero on both, across every tier. There are no account or inactivity fees and no minimum. The cost to plan around is the 1.5 percent currency conversion fee on the base tier.

Trading commissions and the costs that remain

Trading is largely free. The one recurring cost for US investors on the base tier is currency conversion, avoidable by upgrading or by holding Canadian-listed US-exposure ETFs.

| Fee | Rate | Notes |

|---|---|---|

| Stocks and ETFs | $0 | Commission-free online, buying and selling, Canadian and US listed. |

| Options | $0 | No base commission and no per-contract fee, the only broker in Canada at zero on both. |

| Currency conversion | 1.5% | Core tier. About $150 on a $10,000 conversion. Free US dollar account at Premium and Generation. |

| Margin (CAD) | ~5% | Prime plus 0.5% at Core, lower at Premium and Generation. Among the lower rates in the market. |

| Account / inactivity fee | $0 | No administration or inactivity fee, and no minimum to open. |

| US dollar account | $10 / month | Core tier only. Free at the Premium and Generation tiers. |

Where Wealthsimple is not the cheapest

Wealthsimple is cheap on trading but not on currency. On the base Core tier, converting Canadian dollars to US dollars costs 1.5 percent, about $150 on a $10,000 conversion, where Interactive Brokers charges roughly $2. Direct crypto trades also carry a spread rather than a commission, higher than the cost of trading stocks. Heavy US traders who do not want to upgrade tiers will pay more here than at a multi-currency broker.

Is Wealthsimple's Platform Easy to Use?

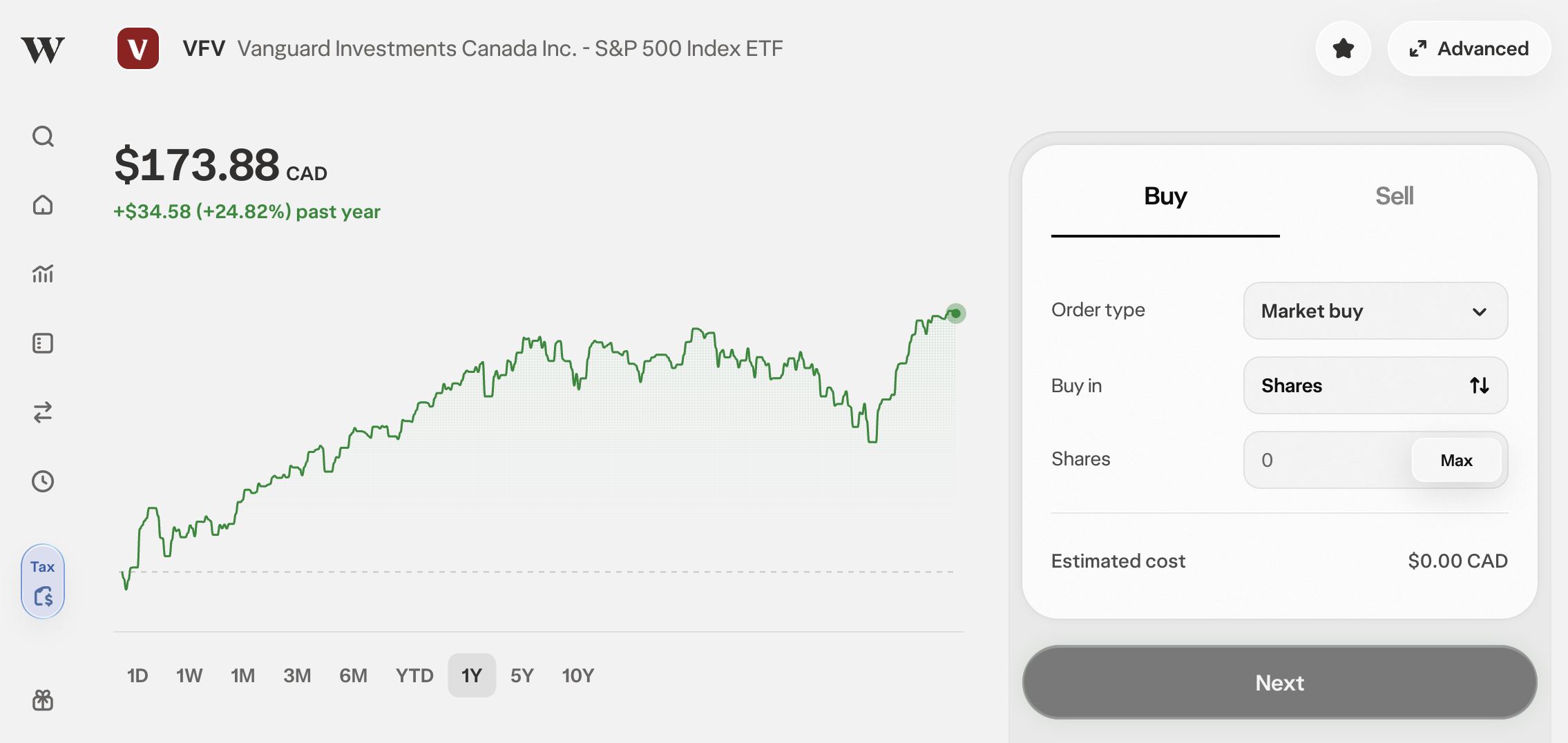

Yes, more than any other broker in Canada. The mobile app is the cleanest and most intuitive in the market, and onboarding is fast, fully digital, and friendly to people who have never invested before. Fractional shares, recurring investing, and direct crypto all live in the same simple interface. The limits are at the advanced end: there is no desktop trading software and the order types are basic.

One platform, built for simplicity rather than active trading.

What Can You Trade with Wealthsimple?

Wealthsimple's lineup is built around what most Canadians actually buy, and it is deliberately narrow. You can trade Canadian and US listed stocks and ETFs commission-free, trade options at no cost, buy fractional shares, and hold cryptocurrency directly, which sets it apart as the only major Canadian broker offering direct crypto rather than just crypto ETFs. What is missing is significant: no bonds, no GICs, no mutual funds, and no international markets beyond Canada and the US.

What Account Types Does Wealthsimple Offer?

Wealthsimple offers a broad registered lineup for a consumer platform: TFSA, RRSP, Spousal RRSP, FHSA, RESP, RRIF, and LIRA, plus cash, margin, and joint accounts, a crypto account, and a chequing-style Cash account. The notable gaps are the RDSP and a formal trust account. There is no minimum to open.

Does Wealthsimple Have Good Research Tools?

This is Wealthsimple's weakest area, and it is a deliberate trade-off. The app gives you basic charting, company profiles, and analyst snapshots, enough to look up a stock and place a trade, but there is no real screener, no deep fundamental data, and none of the professional-grade analytics a research-driven investor expects. For anyone who wants to research before buying, Qtrade and Interactive Brokers are in a different league.

How Is Wealthsimple's Customer Service?

Wealthsimple's support is capable but middle of the pack. You can reach the team by chat, phone, and email, and Premium and Generation clients get priority access, but hours lean toward weekday business times and the 2026 independent service rankings place it in the middle rather than at the top. Most users will not need help often, but if responsive, top-tier service is a priority, Questrade and Qtrade clearly outrank it.

Is Wealthsimple Safe?

Yes. Wealthsimple clears the same regulatory bar as every broker we list, and it is backed by Power Corporation of Canada, serving more than three million clients. As with every broker, protection covers the failure of the firm, not investment losses.

Final Verdict: Should You Open an Account with Wealthsimple?

For most Canadians who are starting out or who want investing to feel as easy as banking, Wealthsimple is the best choice in the country. The app, the onboarding, the $0 options, the low margin, the fractional shares, and the direct crypto add up to an experience nothing else here matches for a mainstream investor. The reasons to look elsewhere are specific and real: if you want bonds, GICs, mutual funds, or international markets, if you rely on serious research, or if you trade US stocks heavily on the base tier and want to dodge the 1.5 percent currency fee, another broker fits better. Research-driven investors should look at Qtrade, and cost-focused or global traders at Interactive Brokers. For everyone who wants the simplest path into investing, Wealthsimple is the easy answer.

Affiliate disclosure: Broker Guide Canada may earn a commission when you open an account through links on this page. See our Disclosures page for more details.

Ready to Open an Account?

Wealthsimple regularly offers a cash bonus when you open and fund an account, and it reimburses the transfer fee your old broker charges. Check the current offer before you sign up.

Our scoring rubric weights affiliate revenue at 0 percent, brokers are ranked on the same categories regardless of commercial relationships. Promo terms current as of June 2026, verify with Wealthsimple before signing up.

Frequently Asked Questions About Wealthsimple

Is Wealthsimple really free?

For trading, largely yes. Canadian and US stocks and ETFs trade commission-free, options cost $0 with no per-contract fee, and there are no account or inactivity fees and no minimum. The main cost is a 1.5 percent currency conversion fee when you trade US securities from a Canadian dollar account, plus a $150 fee if you transfer your account out.

How do I avoid the 1.5 percent currency fee?

Three ways: buy Canadian-listed ETFs that hold US stocks so no conversion happens, hold a US dollar account (free at Premium and Generation, $10 per month at Core) to avoid per-trade conversion, or convert in larger lump sums where reduced tiered rates can apply.

Does Wealthsimple offer options trading?

Yes, and it is the cheapest in Canada. Options trade at $0 with no per-contract fee across every tier. Order types are simpler than a professional platform, but the cost is unbeatable.

Can I buy cryptocurrency on Wealthsimple?

Yes, directly. Wealthsimple is the only major Canadian broker that lets you buy and hold actual crypto rather than only crypto ETFs. Crypto trades carry a spread rather than a commission.

What account types does Wealthsimple offer?

TFSA, RRSP, Spousal RRSP, FHSA, RESP, RRIF, and LIRA on the registered side, plus cash, margin, and joint accounts, a crypto account, and a Cash spending account. It does not offer an RDSP or a formal trust account.

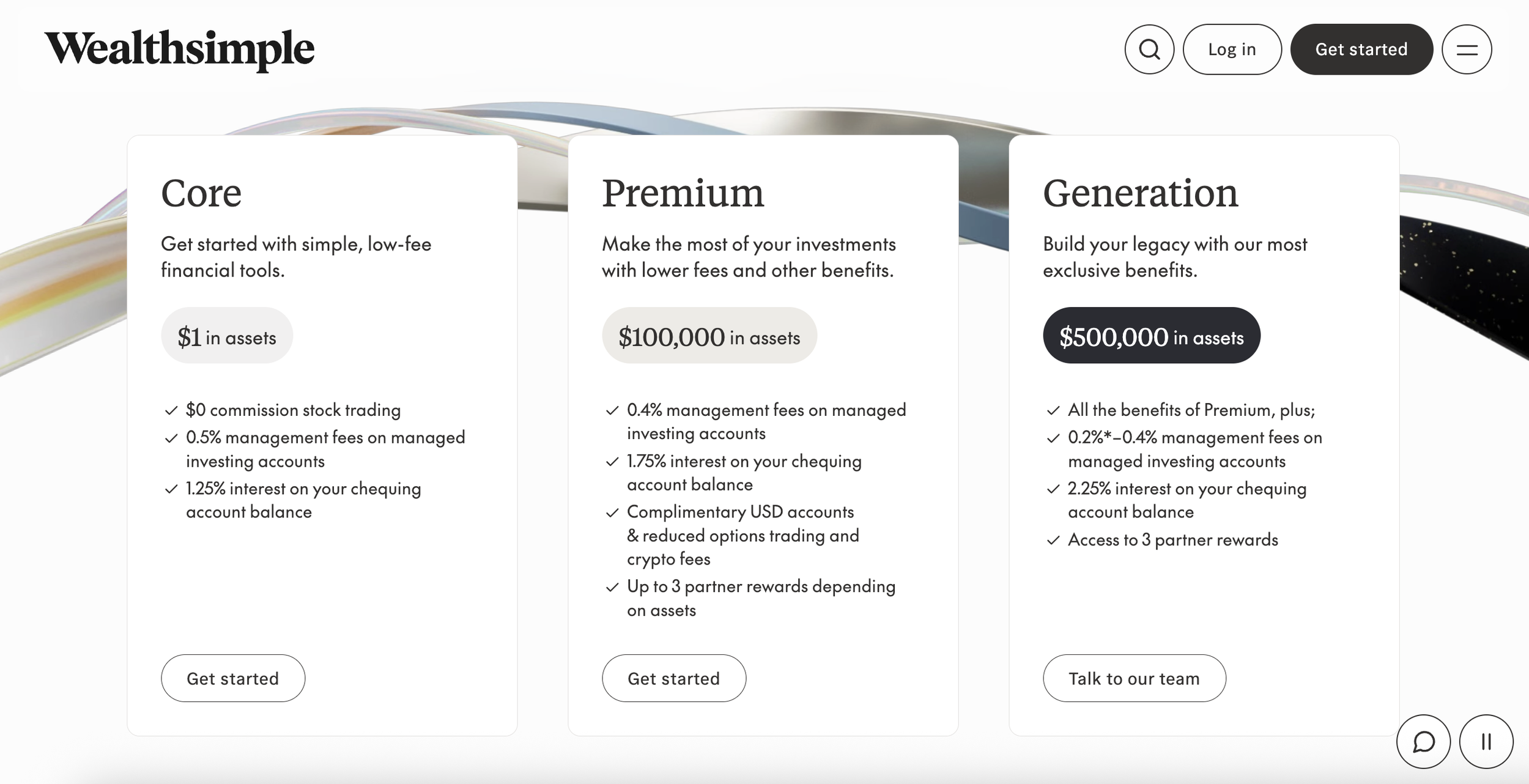

What are the Wealthsimple tiers?

Core for most clients, Premium at $100,000 or more in combined assets, and Generation at $500,000 or more. Higher tiers add a free US dollar account, lower managed-portfolio fees, higher cash interest, and lower margin rates.

Does Wealthsimple have good research tools?

No, this is its weakest area. You get basic charting and company snapshots but no real screener or deep fundamental data. If research matters to you, Qtrade or Interactive Brokers is a much better fit.

How does Wealthsimple compare to Questrade?

Wealthsimple wins on app design, ease, and $0 options; Questrade wins on product range, research, and holding US dollars in registered accounts without a monthly fee. On Canadian ETFs both are commission-free. See the full comparison table to weigh them side by side.